If you read the headlines, you’d think multifamily is struggling. But the underlying data tells a more interesting story.

The U.S. housing market still faces a structural shortage of more than 4 million homes, the result of a decade of underbuilding.

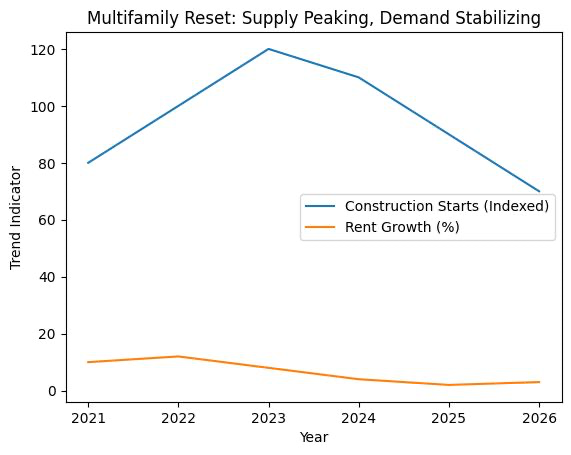

Meanwhile, multifamily construction starts have dropped sharply since 2023 as higher costs and interest rates slowed development.

In other words, while some markets are digesting recent deliveries, future supply is already contracting.

For experienced operators, this is a familiar phase of the cycle.

For LP investors, it’s often where the most disciplined opportunities emerge.

What experienced sponsors are doing differently right now

In today’s environment, strong multifamily investments tend to share a few characteristics:

• Conservative underwriting that assumes normalized rent growth

• Workforce housing focus where demand is durable

• Assets with operational upside, not just appreciation assumptions

• Strong property management partners driving retention and expense control

Across prior ventures, I’ve found that this combination — buying well, operating well, and aligning incentives with investors — consistently produces the most reliable results.

Why many LPs are re-examining multifamily now

For passive investors evaluating their portfolios, multifamily can offer:

• Current income through cash flow

• Inflation-resistant housing demand

• Tax advantages through depreciation strategies

• Diversification away from public markets

But the key difference between average outcomes and strong ones almost always comes down to operator discipline and execution.

A conversation for thoughtful investors

If you’re an accredited investor exploring multifamily as part of a broader portfolio strategy, I’m always happy to share how we evaluate opportunities, structure deals, and align incentives with our LP partners.

Feel free to message me if you’d like to review how we approach underwriting and asset selection.